Table of Content

An insurance binder is required in this situation.Mortgage lenderswill often ask you to prove that you have home insurance. A binder is proof of coverage if you haven’t received your policy documents. It’s a good idea to follow up with your insurance company or agent if your insurance binder is about to expire and you haven’t received your official policy documents. An insurance binder is a temporary contract offering you, the binder holder, insurance coverage while you’re waiting for the formal insurance coverage to kick in.

To learn more about how homeowners insurance can protect your business, get in touch with the independent agents at LoPriore today. Our experienced insurance agents are available 24/7 to answer your questions, provide information about our home insurance policies, or provide you with an instant quote. The owner of the property, also called the policyholder or the named insured, should be clearly listed on the document. If the property is in more than one name, additional owners, such as your spouse, are also listed.

Identity of Insured

As with a car loan, your mortgage lender requires the insurance as a way to protect the collateral’s value, and your ability to repay the loan. Insurers may send insurance binder letters via mail, but if you need proof of bind coverage immediately, you can request electronic delivery through email or fax. Well, yes, except a declaration page is just a summary of your policy and it will generally be issued by your insurance company after the underwriting process is complete. While it’s super easy to put something like a home insurance binder at the end of the list when you’re purchasing a new home, you shouldn’t. It’s essential to have your binder in order or to already have an active policy when you’re trying to close on your home to protect yourself.

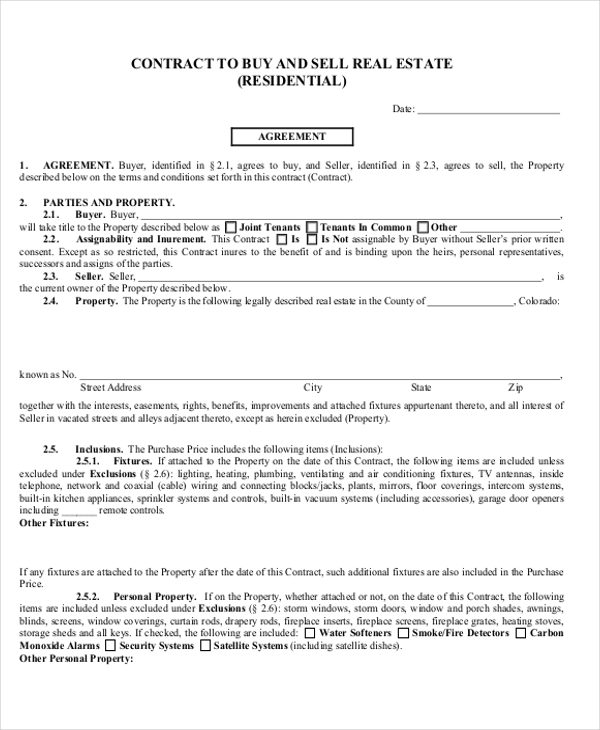

Information About the Insured Property – It must include all the information that you need about our insured property. For example, the location and address of your house and the amount of insurance for the property. If you are ensuring a condo or townhouse, it must include the personal property content. Insured and Mailing Address – The insured or purchaser of the property is listed.

Supplemental Insurance

An insurance binder is essentially a temporary contract that proves that your home insurance provider has agreed to insure your property. The good news is that many insurance policies take minutes to be approved if you’ve applied online. Coverages – The coverages section of the binder is a summary about the specific amount of insurance that your insurance policy provides. This will include the coverage amount on the dwelling, building or structure and the deductible that is on your insurance policy.

Start by looking up how to bind safely, and where to purchase safe binders. Insurance advisors can supply you with a long list of quotes in a few short minutes! This means that you can browse through the best policies from the most respected providers in the country until you've found the perfect match. Hi, I would love to thank Joan LaRochelle for all her assistance with our insurance plans, request and requirements. Jessica Fox has been a freelance writer for five years, with a specialty in health, wellness, and insurance.

Having a hard time finding cheap home insurance in Canada?

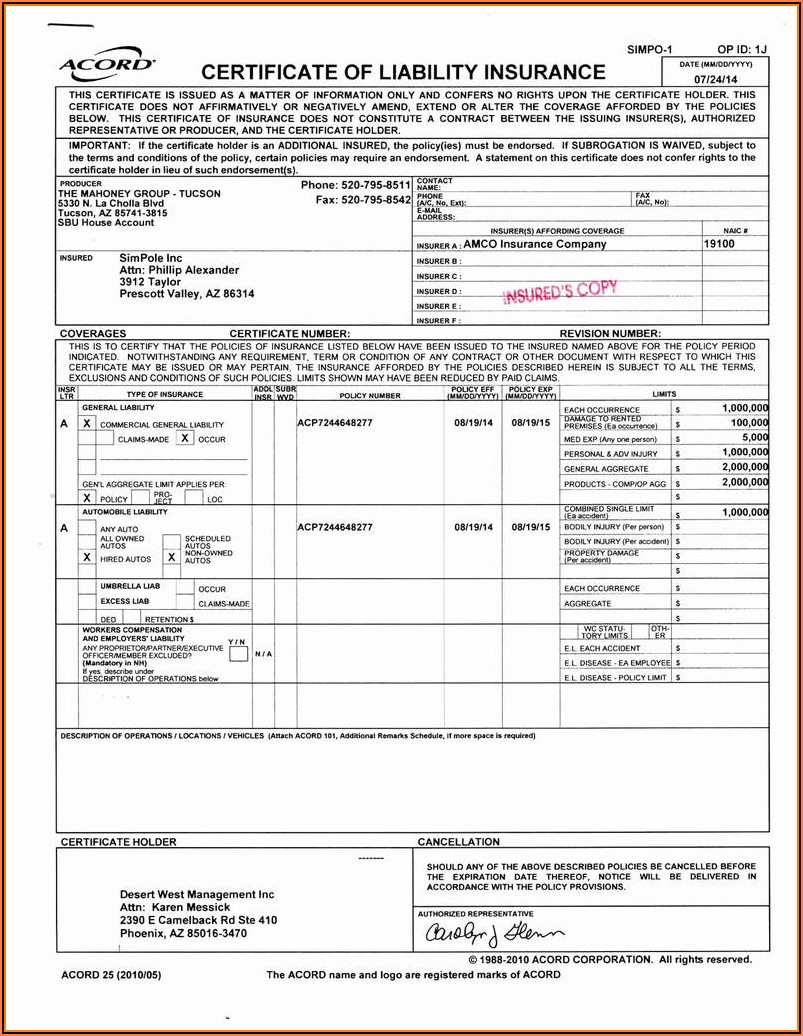

Your insurance binder contains important policy details like coverage limits and deductible amounts. This temporary document outlines the details of your insurance plan and should be provided automatically by your insurance agent. While some details vary, thishomeowners’ insurance binder samplecan give you an idea of what a typical insurance binder looks like.

As a journalist and as an insurance expert, her work and insights have been featured in Forbes Advisor, Kiplinger, Lifehacker, MSN, WRAL.com, and elsewhere. We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. All providers discussed on our site are vetted based on the value they provide. And we constantly review our criteria to ensure we’re putting accuracy first. Founded in 1976, Bankrate has a long track record of helping people make smart financial choices. We’ve maintained this reputation for over four decades by demystifying the financial decision-making process and giving people confidence in which actions to take next.

If you need to provide proof of insurance before receiving your finalized policy, you can utilize your insurance binder letter. Name of Agent – Includes the name of the insurance agent who issued the binder. It also includes a disclaimer indicating that the binder is a subject to the terms and conditions of the policy.

Legal language such as, “subject to policy conditions and exclusions.” This means the binder adheres to the terms of your policy. Your homeowners insurance, for example, may specifically exclude a shed located on your property. The coverage referenced in the binder would then also exclude the shed. Some may even skip the binder by writing a future effective date of coverage, which can still be accepted by mortgage lenders as proof.

The amount of money you will pay out of pocket before the insurance company starts to assist with coverage. Some of the most important information shown on a binder will be the coverage limits of your policy. Also known as a Special Form policy, it will cover both open perils and named perils.

Aninsurance binderis temporary proof of coverage while you wait for the official issuance of yourhomeowner insurance policy. Certain types of insurance coverage are necessary for you to purchase a home. Your insurer will issue you a home insurance binder if you don’t have standard insurance coverage. An insurance binder is temporary proof of coverage and evidence of the insurance policy.

This will be used to repair or rebuild your physical home if it’s damaged or destroyed by a covered loss. An important part of buying a home is figuring out the different types of insurance you may need. A binder is subject to all the terms of the pending contract, unless it is noted otherwise. Samantha Silberstein is a Certified Financial Planner, FINRA Series 7 and 63 licensed holder, State of California Life, Accident, and Health Insurance Licensed Agent, and CFA.